As published in the Palm Coast Observer

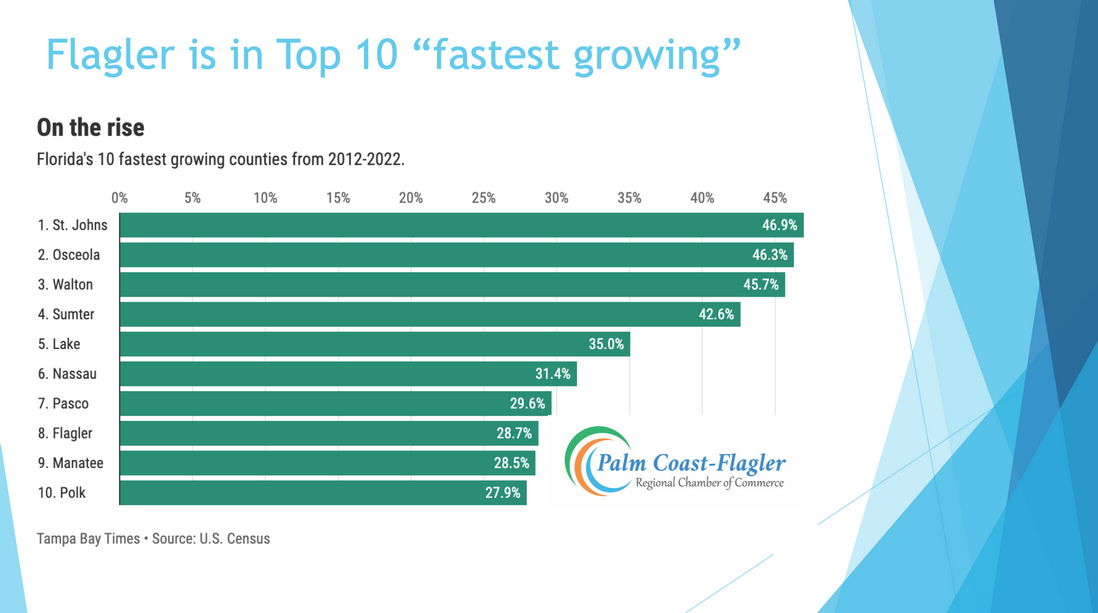

Simply put, population growth has been happening for years (decades even) and will continue for the foreseeable future.

The Palm Coast-Flagler Regional Chamber of Commerce was created, in part, to work collectively build a better economy, create a more prosperous future for our residents and businesses, all while maintaining our region’s high quality of life.

The chamber believes we can seize upon the opportunities provided by a growing community. However, investments must be made.

The growth of the 65+ age demographic indicates investments must be made in local health care services, for example. Investments, such as AdventHealth’s Palm Coast Parkway hospital, have been made in our region. The result has been an additional 1,000 local health care jobs have been added in Flagler since 2019. These high skill, high wage health care jobs pay the type of salary that result in residents being able to afford to live in our community.

Historically, Flagler County’s economy is built on tourism. Today, tourism and retail jobs make up 1/3 of all jobs in our community. Both the tourism and retail industry rely on people spending money. And when people don’t feel good about spending money, or simply don’t have money to spend, our local economy suffers significantly. Tourism will always be a strong part of our economy; however, we need to focus on increasing employment in industries that offer higher wages so our local workers can afford to live locally. Tourism and retail jobs offer among the lowest wages of any local industry sector.

Speaking of living locally, the median price of a single-family home in Flagler County has increased by $140,000 in just the past four years.

Thanks to Internal Revenue Service and moving van company data, we know residents that move from out of state bring significant wealth with them. From 2020-2021, Florida led the nation in net income migration. During that time, new residents brought to Florida $39.2 billion of wealth. Led by residents from New York ($9.8 billion), Illinois ($3.9 billion), New Jersey ($3.8 billion) and California ($3.5 billion), new residents are extremely important to our local economy. Here’s why:

- Approximately 90% of local government ad valorem property tax collections come from residential properties.

- Existing residents’ taxes are capped at a 3% increase each year.

- New residents, typically pay the full tax amount on their property upon purchase.

Because of state law, after a resident has lived in Florida for several years, their capped taxes result in them not paying their fair share of the local tax burden. This is, in part, why new residents are needed. More important, this is why new businesses and investments in our community are needed. After all, commercial properties do not have a tax cap, like residential property. Otherwise, the only way for local governments to gain more revenue is to consider property tax and fee increases.

Infrastructure, and many other public costs, are going up much faster than the 3% tax increase we pay per year as existing residents.

So, what does all this mean?

Our community is changing and growing. We know and can track how it’s changing and growing. If we fail to better position our economy and local governments for the future, our region will continue down a dangerous path that ignores the realities of what’s happening around us. The chamber believes the path to prosperity in our region is better achieved through partnership, planning, strengthening education and investing in our infrastructure.

The PCF Chamber is tracking dozens of community metrics that measure the success of our region. Learn more by visiting www.PCFchamber.com.

Leave a Comment